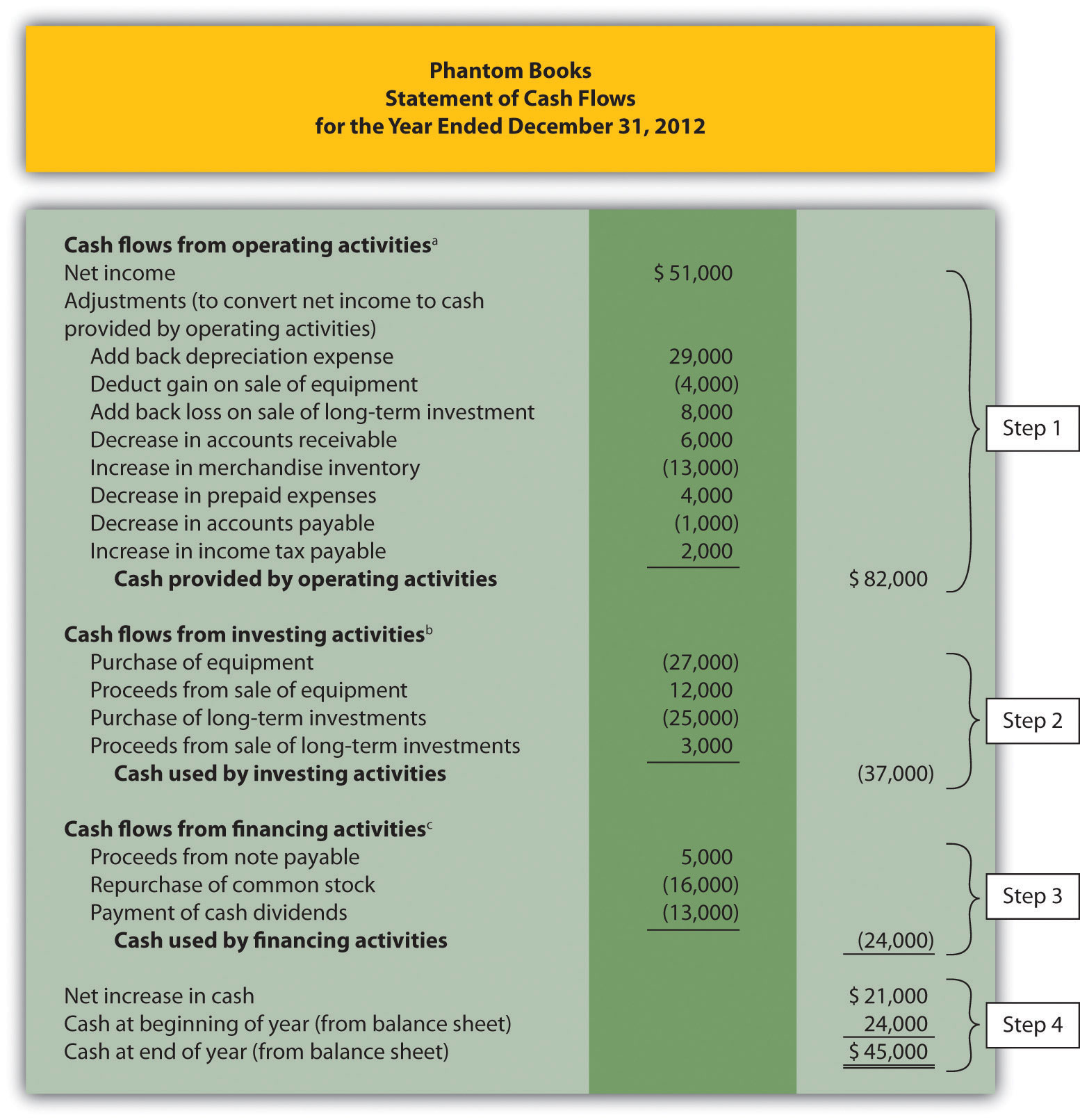

How Is The Statement Of Cash Flows Prepared And Used

What are the total cash flow effects of a decrease in accounts payable. The basic calculation is subtracting ending accounts payable from beginning accounts payable for the period. Then add any increase in inventory in the period or if theres a decrease in inventory deduct this. For example assume that your average daily purchases on account is 300 a day and that your average payable period is 20 days. An increase in accounts payable decreases net income but increases the cash balance when adjusting net income in the cash flow statement. In order to adjust net income to cash flow the increase in accounts receivable for the period must be subtracted from net income. The benefits of extending your average payable period should be crystal clear. Companies need to calculate the increase of decrease in accounts payable prior to including it on the statement of cash flows. A decrease in accounts payable represents that cash has actually been paid to vendorssuppliers. Accrued wages are owed.

Increase in Accounts Payable.

Decrease in accrued liabilities. Thus a decrease in the accounts payable balance represents a decrease in cash and the 919 decrease is subtracted from net income. Decrease in salaries and wages payable. The increase in account payable is always add up with the net income we taken from companys profit loss the logic behind this treatment is the credit sales occurs during the financial year. An increase in accounts payable is a positive adjustment because not paying those bills which were included in the expenses on the income statement is good for a companys cash balance. Increase in Accounts Payable.

Accrued wages are owed. Cash Flows from Operating Activities. In an indirect method the operating activity section of the statement of cash flows starts with the net income. Increase in Accounts Receivable. Cash flow math. Decrease in accrued liabilities. Once thats done deduct any increase in accounts payable in the period or add back any decrease in accounts payable. An Increase in Accounts Payable is Favorable for a Companys Cash Balance It may help to view the positive amounts on the SCF as being favorable or good for a companys cash balance. The increase in account payable is always add up with the net income we taken from companys profit loss the logic behind this treatment is the credit sales occurs during the financial year. Any increase in accruals shall be added to the profit before tax and any decrease in accruals should be subtracted from the profit before tax.

In order to adjust net income to cash flow the increase in accounts receivable for the period must be subtracted from net income. In this case Cash is deducted from Accounts Payable. Decrease in accrued liabilities. Then add any increase in inventory in the period or if theres a decrease in inventory deduct this. An increase in accounts payable decreases net income but increases the cash balance when adjusting net income in the cash flow statement. In an indirect method the operating activity section of the statement of cash flows starts with the net income. Cash flow math. In order to prepare the cash flow statement we adjust the profit before tax with working capital adjustments and operating expenses and accrual is an operating expense payable. An increase in the accounts payable or any current liability account balance is added to net income. Decrease in Income Tax Payable.

Also know How does a decrease in accounts payable affect cash flow. In an indirect method the operating activity section of the statement of cash flows starts with the net income. We start the cash flow from the positive or negative net income. A positive figure represents an increase while a negative number indicates a decrease in the balance. The increase in account payable is always add up with the net income we taken from companys profit loss the logic behind this treatment is the credit sales occurs during the financial year. Decrease in accrued liabilities. In this case Cash is deducted from Accounts Payable. Loss on sale of investments. Decrease in Prepaid Insurance. In order to prepare the cash flow statement we adjust the profit before tax with working capital adjustments and operating expenses and accrual is an operating expense payable.

Decrease in salaries and wages payable. Decrease in accrued liabilities. A decrease in accounts payable would be deducted from net income in determining net cash flow from operations under the indirect method. Add the amount to Net income. Increase in Accounts Receivable. Use the following information regarding the Newcastle Corporation to prepare a statement of cash flows using the indirect method. Accounts payable decrease would mean that it had been paid as is often the case. Increase in Wages Payable. The basic calculation is subtracting ending accounts payable from beginning accounts payable for the period. Then add any increase in inventory in the period or if theres a decrease in inventory deduct this.

A positive figure represents an increase while a negative number indicates a decrease in the balance. Increase in accounts payable 1050 Decrease in wages payable 900 Net cash flow from operating activities 11300 The 8000 includes depreciation and patent expenses. An increase in accounts payable decreases net income but increases the cash balance when adjusting net income in the cash flow statement. And then if there is increase in the account payable during the time for which cash flow statement is preparing. The benefits of extending your average payable period should be crystal clear. Once thats done deduct any increase in accounts payable in the period or add back any decrease in accounts payable. Cash Flows from Operating Activities. The drop in payables would mean a drop in operating cash flow in the statement. Cash flow math. It means the company has paid 100000 to its supplier which is a reduction to cash flow but in effect do.