Simple Prior Period Adjustment Note Disclosure Example Thomas Cook Audit Report

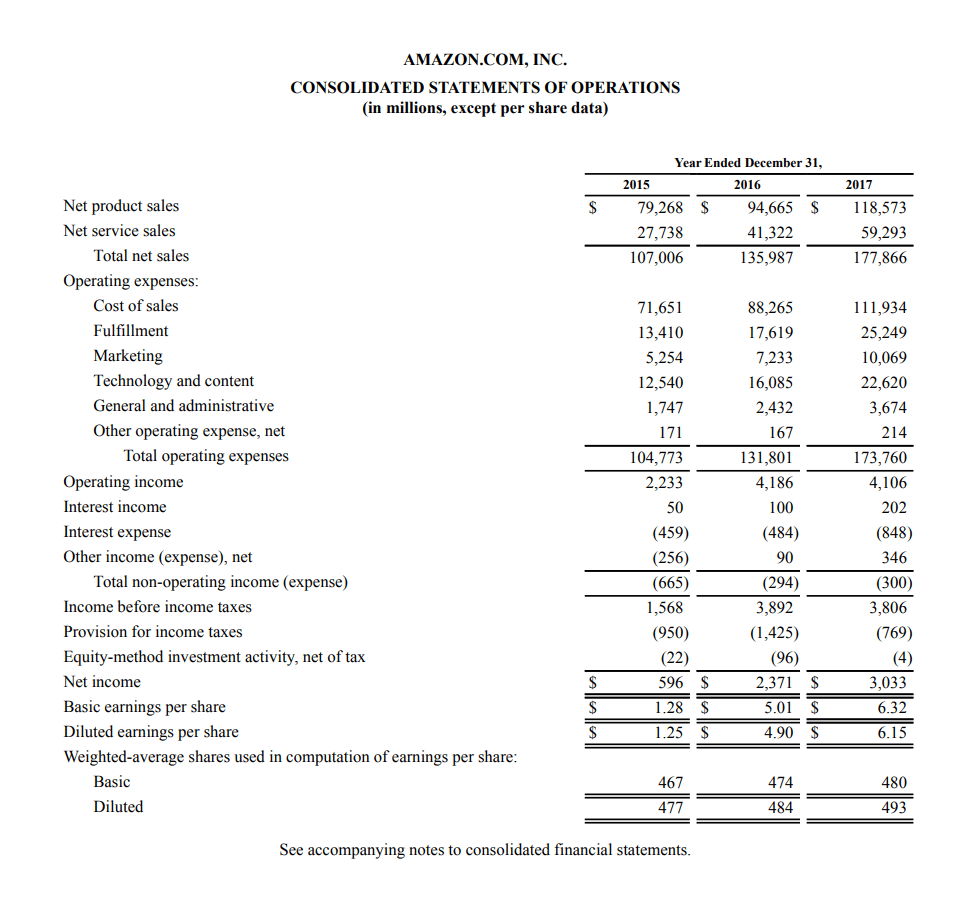

Financial Statements Examples Amazon Case Study

VII Example disclosures for entities that early adopt IFRS 10. Change from an accounting principle that is not generally accepted to one that is generally accepted. Example of Correction of Prior Period Accounting Errors 2 minutes of reading Management of ABC LTD while preparing financial statements of the company for the period ended 31st December 20X2 noticed that they had failed to account for depreciation in last years accounts in respect of an office building acquired in the preceding year. These illustrative financial statements are an example of a group and parent company financial statements prepared for the first time in accordance with FRS 102 The Financial Reporting Standard applicable in the UK and Republic of Ireland. FRS 102 A micro Section 5. Example of a Prior Period Adjustment. These notes are inserted within the relevant section or note. Guidance notes Direct references to the source of disclosure requirements are included in the reference column on each page of the illustrative financial statements. Effect on the amounts reported for the current or prior financial years except as disclosed below1. 269 VIII Example disclosures for interests in unconsolidated structured entities 289 IX Example disclosures for entities that early adopt IFRS 13.

In order to disclose the correction of a prior period errors an agency must disclose the following.

The following is an example of a prior period error highlighting how this could be disclosed in a set of statutory accounts. Net loss gain arising during the period Reclassification adjustment for amortization. What should be in the note. 269 VIII Example disclosures for interests in unconsolidated structured entities 289 IX Example disclosures for entities that early adopt IFRS 13. Provide a description of the nature of the error. Guidance notes Direct references to the source of disclosure requirements are included in the reference column on each page of the illustrative financial statements.

269 VIII Example disclosures for interests in unconsolidated structured entities 289 IX Example disclosures for entities that early adopt IFRS 13. Actual results could differ from those estimates. PRIOR PERIOD ADJUSTMENT DELDOT Fund A prior period adjustment was made to record 2366000 net bond premium discount for DELDOT 2001 and 2002 bond issues restating net assets at June 302002 from 2803953000 to 2806319000. Their preparation involved striking a balance between helpful guidance and burdensome detail. Guidance notes are provided where additional matters may need to be considered in relation to a particular disclosure. In order to disclose the correction of a prior period errors an agency must disclose the following. If the error occurred before the earliest prior period presented restating the opening balances of assets liabilities and equity for the earliest prior period presented. Presents single year financial statements the prior period adjustment affects just the opening balance of retained earnings January 1 2019 in this example. On the consolidated balance sheets income taxes receivable has been. A FRS 103 revised Business Combinations effective for annual periods beginning on or after 1 July 2009 Please refer to note 23aii for the revised accounting policy on business.

Actual results could differ from those estimates. These illustrative financial statements are an example of a group and parent company financial statements prepared for the first time in accordance with FRS 102 The Financial Reporting Standard applicable in the UK and Republic of Ireland. Disclosure of Interests in Other Entities. Guidance notes Direct references to the source of disclosure requirements are included in the reference column on each page of the illustrative financial statements. Adjustments related to prior periods and thus excluded from the operating statements for the current period are limited to. The nature of the prior period errors. And b in government-wide and enterprise funds only other material adjustments which meet the criteria for prior period adjustments contained in GASB Statement 62 Codification of Accounting and Financial Reporting Guidance Contained in Pre. Consolidated Financial Statements IFRS 11. He finds the error in the following year and corrects the error with this entry to the beginning balance of retained earnings. Of prior period errors Dividends declared and payable for the period RETAINED EARNINGS AT 31 DECEMBER 2016 A small company is permitted not to file its profit and loss account or directors report.

Example of Correction of Prior Period Accounting Errors 2 minutes of reading Management of ABC LTD while preparing financial statements of the company for the period ended 31st December 20X2 noticed that they had failed to account for depreciation in last years accounts in respect of an office building acquired in the preceding year. In order to disclose the correction of a prior period errors an agency must disclose the following. We have reclassified certain amounts in prior-period financial statements to conform to the current periods presentation. The company should still provide a disclosure explaining the prior period adjustment. He finds the error in the following year and corrects the error with this entry to the beginning balance of retained earnings. The annexed notes form part of these financial statements. FRS 102 A micro Section 5. Their preparation involved striking a balance between helpful guidance and burdensome detail. These illustrative financial statements are an example of a group and parent company financial statements prepared for the first time in accordance with FRS 102 The Financial Reporting Standard applicable in the UK and Republic of Ireland. 269 VIII Example disclosures for interests in unconsolidated structured entities 289 IX Example disclosures for entities that early adopt IFRS 13.

Consolidated Financial Statements IFRS 11. A FRS 103 revised Business Combinations effective for annual periods beginning on or after 1 July 2009 Please refer to note 23aii for the revised accounting policy on business. If Mountain Bikes Inc. Actual results could differ from those estimates. The following is an example of a prior period error highlighting how this could be disclosed in a set of statutory accounts. On the consolidated balance sheets income taxes receivable has been. Example of a Prior Period Adjustment. Per GASB 62 paragraph 62 when prior period adjustments are recorded the resulting effects are disclosed in the notes to the financial statements. Their preparation involved striking a balance between helpful guidance and burdensome detail. 269 VIII Example disclosures for interests in unconsolidated structured entities 289 IX Example disclosures for entities that early adopt IFRS 13.

Example of a Prior Period Adjustment. And IFRS 12. Change from an accounting principle that is not generally accepted to one that is generally accepted. We have reclassified certain amounts in prior-period financial statements to conform to the current periods presentation. The company should still provide a disclosure explaining the prior period adjustment. If Mountain Bikes Inc. On the consolidated balance sheets income taxes receivable has been. Provide a description of the nature of the error. The nature of the prior period errors. The controller of ABC International makes a mistake when calculating depreciation in the preceding year resulting in depreciation that is 1000 too low.