Casual Reconciliation Of Cost And Financial Accounts Practical Problems Google Balance Sheet

Reconciliation Of Cost And Financial Accounts Introduction Need Objectives Reasons Preparation Procedure Statement Advantages Mcq

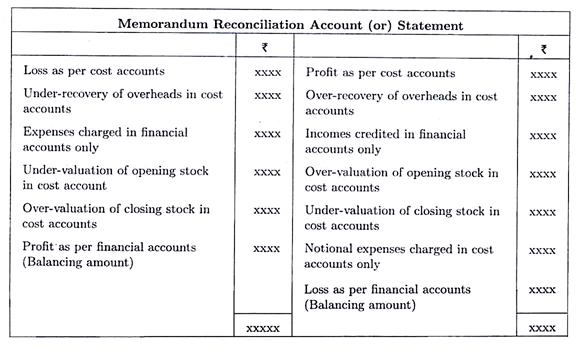

Idle Capacity Cost. Because your company balance sheet reflects all money spentwhether cash credit or loansand all assets purchased with those funds the accuracy of the balance sheet strongly depends on the accurate reconciliation of your companys financial accounts. Quick identification of variances and their type. Reconciliation of Cost and Financial Accounts is the process to find all the reasons behind disagreement in profit which is calculated as per cost accounts and as per financial accounts. Requirements a Write up the ledger accounts for three months. Under the non-integral system of accounting when cost accounts and financial accounts are maintained separately the documents used for ascertaining the amount of expenditure to be charged in respect of some of the items are the same eg cost of materials used and the cost of labour paid are to be ascertained with the help of Material Requisitions and Wages Sheets respectively yet there. Depreciation Machinery by 10 and Amortization of Patents by 20. Job Order Costing Cycle During the month the cost of material purchased was 120000 direct labor cost incurred was 160000 and factory overhead applicable to production was 60000 on April 30 inventories were. Costing Systems Unit and Output Costing Job Costing. However under the integral accounts since cost and financial accounts are integrated into one set of books and only one Profit and Loss Account is prepared the problem of reconciliation does not arise.

Idle Capacity Cost.

It is important to note that the question of reconciliation of cost and financial accounts arises only under non-integral system. C Under-absorption of administrative overheads in cost accounts R 86625- 98000 Profit as per Financial Accounts Illustratio. Ad Intercompany transaction reconciliation solution with extensive traceability. Quick identification of variances and their type. Improve accounting information quality. Reconciliation of Cost and Financial Accounts 7.

The cost accountant of a company has arrived at a profit of 7324150 based on. Idle Capacity Cost. Reconciliation of Cost and Financial Accounts is the process to find all the reasons behind disagreement in profit which is calculated as per cost accounts and as per financial accounts. Because your company balance sheet reflects all money spentwhether cash credit or loansand all assets purchased with those funds the accuracy of the balance sheet strongly depends on the accurate reconciliation of your companys financial accounts. The chief aim is to find out the reasons for the difference between the results shown by Cost Accounts and Financial Accounts. Practical problems in the subject has been explained and wherever necessary practical illustrations. The first step is to compare transactions in the internal register and the bank account to see if the payment and deposit transactions match in both records. Improve accounting information quality. Compare internal cash register to the bank statement. Quick identification of variances and their type.

There are lots of items which are shown in the profit and loss account only when we make it as per financial accounting rules. The reconciliation of cost and financial books can be avoided if the maintenance of two sets of books to cost accounting and financial accounting is dispensed with. Idle Capacity Cost. Costing Systems Unit and Output Costing Job Costing. Practical problems in the subject has been explained and wherever necessary practical illustrations. Improve accounting information quality. RECONCILIATION OF COST AND FINANCIAL ACCOUNTS 10 Hrs Need for Reconciliation Reasons for differences in Profit or Loss shown by Cost Accounts and Profit or Loss. This can be done by adopting integral or integrated accounts in the organisation wherein only one set of books is operated recording both financial and cost accounts. Identify any transactions in the bank statement that are not backed up by any evidence. Under the non-integral system of accounting when cost accounts and financial accounts are maintained separately the documents used for ascertaining the amount of expenditure to be charged in respect of some of the items are the same eg cost of materials used and the cost of labour paid are to be ascertained with the help of Material Requisitions and Wages Sheets respectively yet there.

Labour Hour Rate 6. Job Cost Cards Collecting Direct Costs. Requirements a Write up the ledger accounts for three months. Reconciliation of Cost and Financial Accounts 7. Inventory on 31 st December 2015 was valued at Rs. Reasons for the Difference. Ad Intercompany transaction reconciliation solution with extensive traceability. C Under-absorption of administrative overheads in cost accounts R 86625- 98000 Profit as per Financial Accounts Illustratio. Practical problems in the subject has been explained and wherever necessary practical illustrations. In this article we have compiled various cost accounting problems along with its relevant Solutions.

Identify any transactions in the bank statement that are not backed up by any evidence. Reasons for the Difference. Job Cost Cards Collecting Direct Costs. Reconciling accounts and comparing transactions also helps your accountant produce reliable accurate and high-quality financial statements. After reading this article you will learn about cost accounting problems on. Under the non-integral system of accounting when cost accounts and financial accounts are maintained separately the documents used for ascertaining the amount of expenditure to be charged in respect of some of the items are the same eg cost of materials used and the cost of labour paid are to be ascertained with the help of Material Requisitions and Wages Sheets respectively yet there. Prepare Bank Reconciliation Statement for the month of December 2007 by missing method using T accounts for cash book and for bank statement and Reconciliation. Method Absorption of Factory Overheads Methods of Absorption Machine Hour Rate Problems. The cost accountant of a company has arrived at a profit of 7324150 based on. Practical problems in the subject has been explained and wherever necessary practical illustrations.

Job Order Costing Cycle During the month the cost of material purchased was 120000 direct labor cost incurred was 160000 and factory overhead applicable to production was 60000 on April 30 inventories were. Because your company balance sheet reflects all money spentwhether cash credit or loansand all assets purchased with those funds the accuracy of the balance sheet strongly depends on the accurate reconciliation of your companys financial accounts. The reconciliation of cost and financial books can be avoided if the maintenance of two sets of books to cost accounting and financial accounting is dispensed with. However under the integral accounts since cost and financial accounts are integrated into one set of books and only one Profit and Loss Account is prepared the problem of reconciliation does not arise. After reading this article you will learn about cost accounting problems on. Requirements a Write up the ledger accounts for three months. Inventory on 31 st December 2015 was valued at Rs. A Over-valuation of closing stock in cost account b Under-absorption of direct wages in cost accounts 2 18800 -. The cost accountant of a company has arrived at a profit of 7324150 based on. Labour Hour Rate 6.