Prepare Statement Of Partners Capital Assume That Chegg Com

For example assume Dees Consultants Inc a partnership earned 60000 and their agreement is that all profits are shared equally. We are a leading international outsourced investment office with a mission to. Partner capital components are the parts of the total Partners Capital balance including that which is allocated to accumulated other comprehensive income comprehensive income. Statement of partners equity. The taxpayer needs to attach a statement to the partners Schedule K-1 indicating the method used to determine each partners capital account. The division is shown in the statement of division of profit. Each of the three partners would be allocated 20000 60000 3. It is important to note that partners salaries and interest on capital are not charges in the main part of the Income statement. Format C - 3 partners max. Format B - 5 partners max.

Amount of incentive obligation paid in cash or stock during the period to a limited liability corporation managing member or limited partnership general partner.

Prepare a statement of partnership liquidation indicating a the sale of assets and division of loss b the payment of liabilities c the receipt of the deficiency from the appropriate partner and d the distribution of cash. Assume that the partner with the capital deficiency declares bankruptcy and is unable to pay the deficiency. The total amount of distributions to limited partners. We are a leading international outsourced investment office with a mission to. Partner C was admitted to the partnership during the year with a capital. The statement starts with the beginning capital.

It has the same format as the statement of owners equity except that it includes a column for each partner and a total column for the company rather than just one column. The partnership capital account is an equity account in the accounting records of a partnership. The total amount of distributions to limited partners. Tax Basis Method Partnerships that have always reported using the tax basis method for partners capital should continue using that method. The taxpayer needs to attach a statement to the partners Schedule K-1 indicating the method used to determine each partners capital account. ASC 946-205-45-1 Statement of changes in partners capital and 5 Year ended December 31 20XX ASC 946-505-50-2 Limited ASC 946-505-50-3 General partner partners Total Partners capital beginning of year 75884000 682957000 758841000 Capital contributions 250000 24750000 25000000 Capital distributions 373000 36888000 37261000. They are simply part of the process of dividing up the profit among the partners. Statement of Assets Liabilities and Partners Capital December 31 20XX See accompanying notes to financial statements. In other words its a financial statement that reports the increases and decreases in the partners accounts over the course of a period. 2 Private investment companies are permitted to present partners capital as a single caption.

For example assume Dees Consultants Inc a partnership earned 60000 and their agreement is that all profits are shared equally. The total amount of distributions to limited partners. Partners Capital Account Distributions. The statement of capital provides a snapshot of a companys share capital at a certain date showing the different share classes that exist the amounts invested and the rights attached to shares issued. The statement starts with the beginning capital. Partner capital components are the parts of the total Partners Capital balance including that which is allocated to accumulated other comprehensive income comprehensive income. ASC 946-205-45-1 Statement of changes in partners capital and 5 Year ended December 31 20XX ASC 946-505-50-2 Limited ASC 946-505-50-3 General partner partners Total Partners capital beginning of year 75884000 682957000 758841000 Capital contributions 250000 24750000 25000000 Capital distributions 373000 36888000 37261000. The statement of partners capital is a financial report that shows the changes in total partners capital accounts during an accounting period. Profits and losses earned by the business and allocated. Statement of changes in partners capital Year ended December 31 20XX General partner Limited partners Total Partners capital beginning of year 75884000 682957000 758841000 Capital contributions 250000 24750000 25000000 Capital distributions 373000 36888000 37261000 Allocation of net income 1.

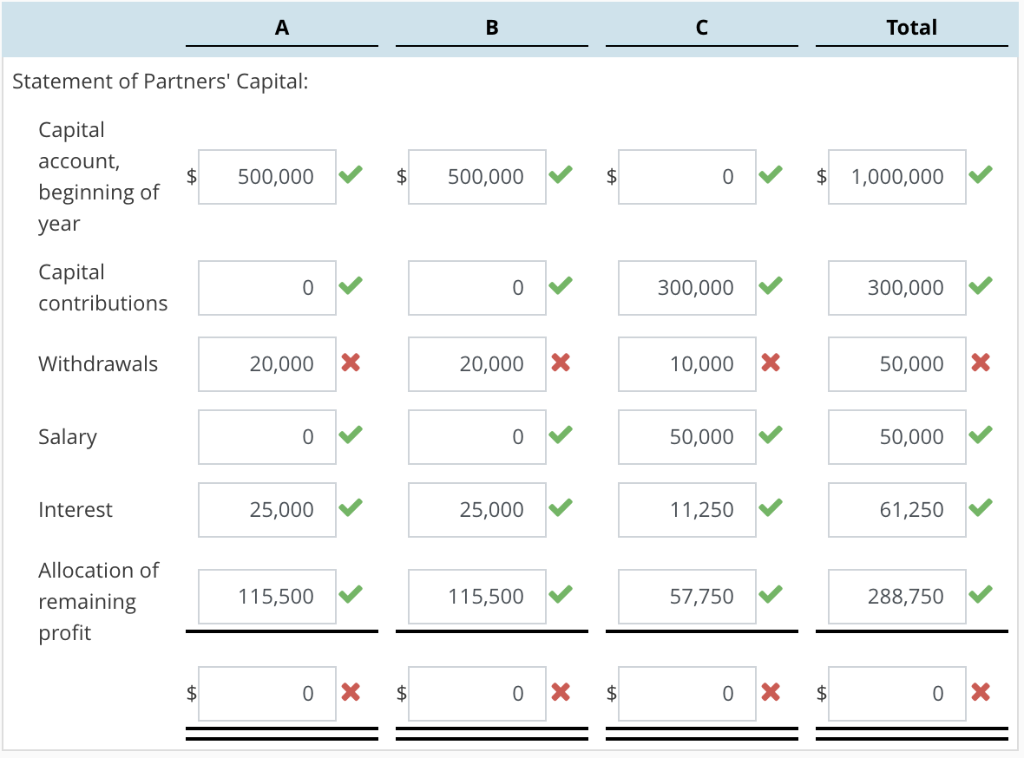

1 Refer to guidance in ASC 505-10-45-2 to determine classification of capital contributions receivable as an asset or as a reduction of partners capital. Partner capital components are the parts of the total Partners Capital balance including that which is allocated to accumulated other comprehensive income comprehensive income. Prepare statement of partners capital Assume that there are three partners in a partnership A B and C. Partners Capital is an Outsourced Investment Office acting for highly regarded endowments and foundations senior partners at leading global investment firms and sophisticated ultra-high-net-worth families in Europe North America and Asia. The statement starts with the beginning capital. It is important to note that partners salaries and interest on capital are not charges in the main part of the Income statement. Partners A and B each began the year with a capital account of 500000. The division is shown in the statement of division of profit. 2 Private investment companies are permitted to present partners capital as a single caption. Partner Type of Partners Capital Account Name.

The Partnership Agreement provides for a salary to Partner C of 50000 and. Partner C was admitted to the partnership during the year with a capital. Format A - Current and prior year. Partners A and B each began the year with a capital account of 500000. ASC 946-205-45-1 Statement of changes in partners capital and 5 Year ended December 31 20XX ASC 946-505-50-2 Limited ASC 946-505-50-3 General partner partners Total Partners capital beginning of year 75884000 682957000 758841000 Capital contributions 250000 24750000 25000000 Capital distributions 373000 36888000 37261000. Amount of incentive obligation paid in cash or stock during the period to a limited liability corporation managing member or limited partnership general partner. It is important to note that partners salaries and interest on capital are not charges in the main part of the Income statement. This may be presented in a tabular format as shown in the next section. A partnership usually prepares a financial document known as the statement of partners capital. This document details the contributions of each partner and the balance of each partners equity in the business over a period of time usually one year.

It has the same format as the statement of owners equity except that it includes a column for each partner and a total column for the company rather than just one column. It contains the following types of transactions. Profits and losses earned by the business and allocated. Partners Capital is an Outsourced Investment Office acting for highly regarded endowments and foundations senior partners at leading global investment firms and sophisticated ultra-high-net-worth families in Europe North America and Asia. Instead companies limited by shares must maintain and in certain circumstances submit to Companies House the statement of capital. The total amount of distributions to the general partner during the period. Additional investments and allocated net income increase capital accounts of the partners. Statement of partners equity. Once net income is allocated to the partners it is transferred to the individual partners capital accounts through closing entries. This document details the contributions of each partner and the balance of each partners equity in the business over a period of time usually one year.